Bitcoin and the global economy are inextricably linked. The crypto coin has been developed as a counter-reaction to the economic crisis of 2008. For many, bitcoin therefore serves as a Plan ฿.

At the moment it seems to be going well economically, but more and more signs point to a new recession. From today, therefore, we explain a topic from the macro-economy every Tuesday. So we don’t forget why bitcoin was developed.

We continue this series with the ever-falling savings rates. You may not notice it now, but actually your money slowly evaporates when you leave it in the bank. In this article you can read why.

Savings interest rates are getting lower

The falling interest rate is intended as an incentive. The European Central Bank (ECB) wants to make it unattractive to save and wants Europeans to spend more. But now there is little room left to lower interest rates, which is now almost 0 percent.

The data from the chart below comes from De Nederlandsche Bank, the central bank of the Netherlands:

The top blue line represents the interest on deposit accounts. You open a deposit if you want to secure your money for a longer period of time. The disadvantage is that you cannot access your money until the end of the term. The advantage is the higher interest. Although high, on average the interest for a deposit account is now 2.19 percent. That is about as high as a normal savings account in December 2009.

On the bottom line you can see the interest on regular savings accounts. The average savings interest is now historically low, only 0.09 percent. Only just in the plus so. And even that is no longer certainty.

Indeed, there are now even savings accounts with no interest. Triodos bank had the dubious honor of being the first bank with an interest rate of 0 percent. You read that right, no interest at all. Van Lanschot also no longer charges savings.

The deposit rate of the European Central Bank is currently -0.5 percent. Banks who want to deposit short-term money at the ECB must deposit money for this. This sparks a whole new discussion, namely when does this affect us?

When will there be negative savings rates in the Netherlands?

A negative interest rate is a major psychological step. Banks prefer to postpone this step to retain customers. The step of Triodos not to charge interest is therefore daring in that regard. In Belgium, negative interest rates are even completely prohibited.

Yet it can just happen that a Dutch bank will charge a negative interest rate. At the end of September, Minister of Finance Wopke Hoekstra said that he did not intend to introduce such a ban on negative interest. “A negative savings interest for consumers is not yet an issue,” he reasons.

But there are banks that play with this idea. For example, ING CEO Ralph Hamers is considering introducing a negative interest rate on savings. Or yes, at least he does not exclude it: “The question is: are you going to count negative interest on savings or are there other ways to compensate.”

De Volksbank also does not exclude a negative interest rate: “It is clear that nobody wants a negative interest rate. The savers don’t want that, the banks don’t want that. But you can never exclude anything. “

Why is the negative interest rate problematic?

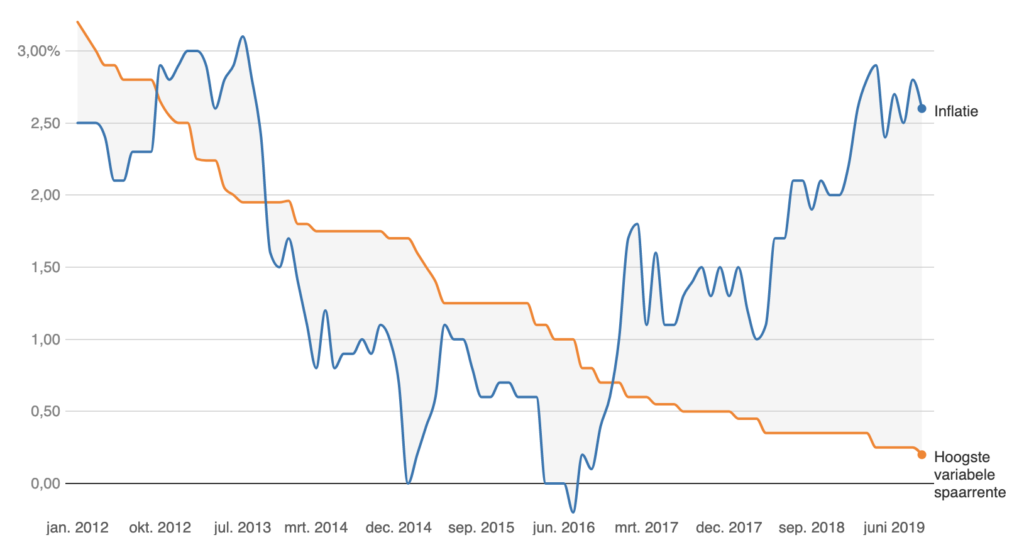

That interest rates fall is not the only problem. Meanwhile, the prices of products continue to rise, that is called inflation. Inflation in the Netherlands in September 2019 was 2.6 percent, a lot higher than the savings rate.

In other words, you actually hand in money by leaving your money in the bank. You can see that well on the graph below. You see the savings interest rate (orange) compared to inflation (blue):

This ratio has been skewed since December 2016. But because you still receive interest on your savings account, it is not surprising that you are secretly throwing your money away. A negative savings account only sounds more alarming.

What if there is a negative savings interest?

What do Dutch people do if there is a negative interest rate? The Netherlands Authority for the Financial Markets has investigated this. Only 12 percent would leave the savings in a freely withdrawable savings account. Others chose:

- Physical storage (the well-known “old sock”) (34%)

- Investing (20%)

- Pay off debts (18%)

- Save deposit (11%)

- Publishing (5%)

But the AMF has forgotten something. There is a currency in which you neither receive interest nor have to pay if you save it. With bitcoin you are not dependent on the policy of the central bank. You are your own bank, you decide for yourself what happens with your bitcoin.

The Return On Investment from bitcoin is a good benchmark. If you bought bitcoin last year, you would have achieved a return of more than 30 percent. That sounds better than saving your money in an old sock!

Related posts:

GitHub Libra Code draws criticism from users

GitHub Libra Code draws criticism from users  Tipping on Reddit and Vimeo in BAT introduced by Brave

Tipping on Reddit and Vimeo in BAT introduced by Brave  Newcomers to the crypto market have to pay attention to scams and pump and dumps

Newcomers to the crypto market have to pay attention to scams and pump and dumps  Hardly any growth in downloaded crypto apps, despite tripling price bitcoin

Hardly any growth in downloaded crypto apps, despite tripling price bitcoin  Bloomberg accepts Bitcoin – says cryptomonads are here to stay

Bloomberg accepts Bitcoin – says cryptomonads are here to stay  The Central Bank can release their cryptocurrencies earlier than expected

The Central Bank can release their cryptocurrencies earlier than expected